Open Strategist

Sunday, March 30, 2014

Saturday, March 29, 2014

Weekend Links

Advice for a Happy Life by Charles Murray - WSJ.com: http://t.co/DPzUXTO via @AddThis

Big data: are we making a big mistake? - FT.com: http://t.co/DT9vDgX via @AddThis

State of Journalism: The Lost Art of Fact Checking | LinkedIn: http://t.co/yRiZtQZ via @AddThis

How Busy People Make Time To Read--And You Can Too | Fast Company | Business + Innovation: http://t.co/kILRQAU via @AddThis

Kindergarten teacher: My job is now about tests and data — not children. I quit.: http://t.co/8SslZPs

Blue Bottle coffee: VCs’ search for the new Starbucks starts in San Francisco.: http://t.co/DAsipkh

There’s No Substitute for Good Judgment | Above the Market: http://t.co/EOLSVTI via @AddThis

The March Madness Vasectomy «: http://t.co/UPydEme via @AddThis

What I learned from negotiating with Steve Jobs: http://t.co/6CvM20i via @AddThis

Videos:

Why did CEO pay got out of hand ? Buffet on youtube

Parasite Rex: Inside the Bizarre World of Nature's Most Dangerous Creatures

Jim Grant lecture: Hazlitt, My Hero Youtube

Big data: are we making a big mistake? - FT.com: http://t.co/DT9vDgX via @AddThis

State of Journalism: The Lost Art of Fact Checking | LinkedIn: http://t.co/yRiZtQZ via @AddThis

How Busy People Make Time To Read--And You Can Too | Fast Company | Business + Innovation: http://t.co/kILRQAU via @AddThis

Kindergarten teacher: My job is now about tests and data — not children. I quit.: http://t.co/8SslZPs

Blue Bottle coffee: VCs’ search for the new Starbucks starts in San Francisco.: http://t.co/DAsipkh

There’s No Substitute for Good Judgment | Above the Market: http://t.co/EOLSVTI via @AddThis

The March Madness Vasectomy «: http://t.co/UPydEme via @AddThis

What I learned from negotiating with Steve Jobs: http://t.co/6CvM20i via @AddThis

Videos:

Why did CEO pay got out of hand ? Buffet on youtube

Parasite Rex: Inside the Bizarre World of Nature's Most Dangerous Creatures

Jim Grant lecture: Hazlitt, My Hero Youtube

Friday, March 28, 2014

Friday, March 21, 2014

Weekend Longform Links

- "Nate Silver and the Emptiness of Data Journalism" http://rdd.me/em9rzh6g via @readability

- "The Scottish pound myth" http://rdd.me/fklunf0r via @readability

- "The slow death of the microwave" http://rdd.me/szpmr0vt via @readability

- "No, Nate, brogrammers may not be macho, but that’s not all there is to it" http://rdd.me/ga7orrob via @readability

- "The Secret World of Fast Fashion" http://rdd.me/n60qkqkj via @readability

- "Hoard d’Oeuvres" http://rdd.me/ljgule2p via @readability

- "Excerpts from Mosaic: Perspectives on Investing (Mohnish Pabrai)" http://rdd.me/hl6lvem6 via @readability

- "The Paradox of Self-Determination" http://rdd.me/fchwurln via @readability

- "Can TOMS break into the coffee business? - Fortune Features" http://rdd.me/wkx2bwmw via @readability

- "An Interview with WiseBanyan CEO Herbert Moore" http://rdd.me/kzhswidt via @readability

Thursday, March 20, 2014

FW: Tanker Tracker

Feed: The Big Picture

Posted on: Thursday, March 20, 2014 11:30

Author: Barry Ritholtz

Subject: Tanker Tracker

|

|

Tuesday, March 18, 2014

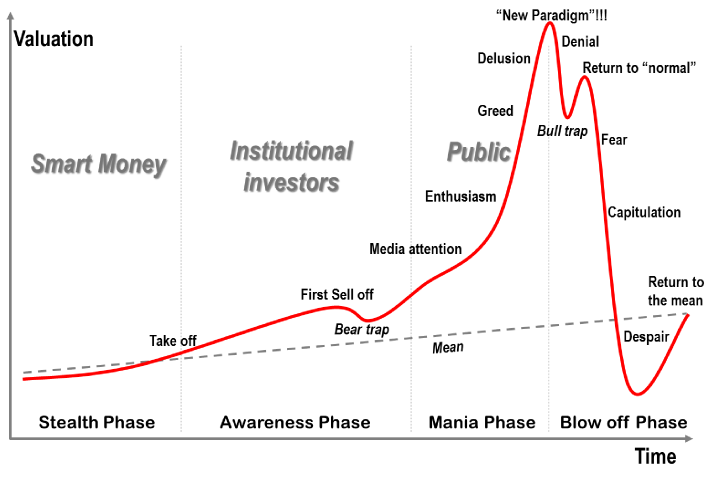

FW: Where Are We in the Bubble and Mania Cycle?

| Bubbles and Manias Josh Brown reminded us yesterday of this terrific chart from Jean-Paul Rodrigue, a professor in the department of global studies and geography Department at Hofstra University. Of course, the key question is: Where are we on the chart? My view is that we're through the "Awareness" phase as many of the bears have already thrown in the towel (Jeremy Grantham is the latest one). |

Monday, March 17, 2014

Sunday, March 16, 2014

Saturday, March 15, 2014

Weekend Longform Links

The Future of Internet Freedom http://nyti.ms/1quep4O

My Life as a Retail Worker: Nasty, Brutish, and Poor - Joseph Williams - The Atlantic

My Life as a Retail Worker: Nasty, Brutish, and Poor - Joseph Williams - The Atlantic

Elizabeth Kolbert: When Grownups Take the SAT NewYorker

The complete guide to listening to music at work – Quartz

"The Infinite Lives Of BitTorrent" http://rdd.me/yuvuueop via @readability

Are Malls Over? NYT

They come here, taking our jobs... Worried about immigration? Wait till I tell you about young people Newstatesment

"The Gavel Drops at Sotheby’s" http://rdd.me/ub1gwzjd via @readability

"Haiti’s Shadow Sanitation System" http://rdd.me/szkcjeue via @readability

"Nate Silver on the Launch of ESPN’s New FiveThirtyEight, Burritos, and Being a Fox" http://rdd.me/dm8cpnni via @readability

"Why We're Awful at Assessing Risk" http://rdd.me/qoxu7mjh via @readability

"An Investor’s Guide to Better Writing — Seriously" http://rdd.me/ddueuoar via @readability

"Missed Alarms and 40 Million Stolen Credit Card Numbers: How Target Blew It" http://rdd.me/t9p71ocx via @readability

"Reading reinvented for mobile era" http://rdd.me/04xfbtgc via @readability

"Technology: Rise of the replicants - FT.com" http://rdd.me/z6eicnuj via @readability

"The Story Behind the SAT Overhaul" http://rdd.me/rwvuwwgk via @readability

Billionaire Activist Steyer: Titans at the Table via @BloombergTV http://bloom.bg/1dMK8nQ

General Of The Army, Omar Bradley, January 23, 1981 (full): http://youtu.be/fDSrf3cosbo via @YouTube

Listened to Podcast Episode #25: Shane Parrish from The Web Psychologist » Blog @Stitcher http://www.stitcher.com/s?eid=32894783

The complete guide to listening to music at work – Quartz

"The Infinite Lives Of BitTorrent" http://rdd.me/yuvuueop via @readability

Are Malls Over? NYT

They come here, taking our jobs... Worried about immigration? Wait till I tell you about young people Newstatesment

"The Gavel Drops at Sotheby’s" http://rdd.me/ub1gwzjd via @readability

"Haiti’s Shadow Sanitation System" http://rdd.me/szkcjeue via @readability

"Nate Silver on the Launch of ESPN’s New FiveThirtyEight, Burritos, and Being a Fox" http://rdd.me/dm8cpnni via @readability

"Why We're Awful at Assessing Risk" http://rdd.me/qoxu7mjh via @readability

"An Investor’s Guide to Better Writing — Seriously" http://rdd.me/ddueuoar via @readability

"Missed Alarms and 40 Million Stolen Credit Card Numbers: How Target Blew It" http://rdd.me/t9p71ocx via @readability

"Reading reinvented for mobile era" http://rdd.me/04xfbtgc via @readability

"Technology: Rise of the replicants - FT.com" http://rdd.me/z6eicnuj via @readability

"The Story Behind the SAT Overhaul" http://rdd.me/rwvuwwgk via @readability

Billionaire Activist Steyer: Titans at the Table via @BloombergTV http://bloom.bg/1dMK8nQ

General Of The Army, Omar Bradley, January 23, 1981 (full): http://youtu.be/fDSrf3cosbo via @YouTube

Listened to Podcast Episode #25: Shane Parrish from The Web Psychologist » Blog @Stitcher http://www.stitcher.com/s?eid=32894783

Friday, March 14, 2014

FW: Banker’s bloat

| Wall Street bonuses are increasing again "GREED is good!" boomed Michael Douglas in the 1987 film "Wall Street." Though an anthem of the perceived excesses of the time, the bonuses then forked out to financiers were relatively meager: $32,000 on average. The sum would grow four-fold in the 1990s. And then it soared higher still, reaching a peak just before the financial crisis. In 2006 New York's investment banks paid nearly $40 billion in bonuses (adjusted for inflation)—about ten times the budget of the United Nations. During the crisis, banks had to show contrition and bonuses halved. But they have restarted their ascent. In 2013 the bonus pool of New York's financial-sector employees increased 15% to about $27 billion, as discussed in an item from this week's issue here. |

Wednesday, March 12, 2014

Tom Sawyer and psychology

In a famous passage of Mark Twain’s novel Tom Sawyer, Tom is faced

with the unenviable job of whitewashing his aunt’s fence in full view of his friends

who will pass by shortly and whose snickering promises to add insult to injury.

When his friends do show up, Tom applies himself to the paintbrush with gusto,

presenting the tedious chore as a rare opportunity. Tom’s friends wind up not only

paying for the privilege of taking their turn at the fence, but deriving real pleasure

from the task—a win–win outcome if there ever was one. In Twain’s words, Tom

“had discovered a great law of human action, without knowing it—namely, that in

order to make a man or a boy covet a thing, it is only necessary to make the thing

difficult to attain.”

via:DUKE

with the unenviable job of whitewashing his aunt’s fence in full view of his friends

who will pass by shortly and whose snickering promises to add insult to injury.

When his friends do show up, Tom applies himself to the paintbrush with gusto,

presenting the tedious chore as a rare opportunity. Tom’s friends wind up not only

paying for the privilege of taking their turn at the fence, but deriving real pleasure

from the task—a win–win outcome if there ever was one. In Twain’s words, Tom

“had discovered a great law of human action, without knowing it—namely, that in

order to make a man or a boy covet a thing, it is only necessary to make the thing

difficult to attain.”

via:DUKE

Tuesday, March 11, 2014

FW: Safe skies

| Despite a recent tragedy, air flights are getting safer THE disappearance of flight MH370, which lost contact with air-traffic control between Kuala Lumpur and Beijing, is a reminder of the dangers of air travel. Yet thankfully, such disasters are exceedingly rare. Over the past four decades fatalities on aeroplanes—be it from accidents or terrorism—have declined even as the number of travellers has increased almost ten-fold. Aviation is also much safer than other forms of transport. On a per passenger-mile basis, an individual is about 180 times more likely to die in a car than on a plane, according to America's National Safety Council (though these types of travel are not in direct competition). As for flight MH370, the mysteriousness is heightened because the aircraft vanished while cruising. It is a phase of flight that accounts for only 9% of fatalities but almost 60% of time spent in the air, according to the Aviation Safety Network, an independent database in the Netherlands. |

Sunday, March 9, 2014

Wednesday, March 5, 2014

Six points from Man Searching for Meaning

1. “The one thing you can’t take away from me is the way I choose to respond to what you do to me. The last of one’s freedoms is to choose one’s attitude in any given circumstance.”

2. “Those who have a 'why' to live, can bear with almost any 'how'.”

3. “An abnormal reaction to an abnormal situation is normal behavior.”

4. “Life is never made unbearable by circumstances, but only by lack of meaning and purpose.”

5. “The attempt to develop a sense of humor and to see things in a humorous light is some kind of a trick learned while mastering the art of living.”

6. “We cannot, after all, judge a biography by its length, by the number of pages in it; we must judge by the richness of the contents...Sometimes the 'unfinisheds' are among the most beautiful symphonies.”

Via: GR

Tuesday, March 4, 2014

Monday, March 3, 2014

Polymath = success ?

I think we need to realize that we should all be targeting to be a polymath someday…

Rather like giving up the Economist podcast, this epiphany came as a sort of liberation. “The best thing is that I now idolise polymaths, people like da Vinci and Michelangelo,” he says. “They weren’t just engineers, they were artists and scientists, mathematicians and philosophers. They weren’t even experts in their own domain. Their genius lay in piecing things together.”

Via: FT

God Created the world - JP Morgan reorganized it

1901: J.P. Morgan announces that he is organizing the largest corporation the world has yet seen by merging his Federal Steel conglomerate with Andrew Carnegie’s Carnegie Co. The company is initially capitalized at $1.4 billion -- the first billion-dollar company ever -- four times the budget of the U.S. government and 7% of the gross national product. In a popular joke of the day, a schoolboy is asked about the history of the world. "God created the world in 4004 B.C.," he answers, "and it was reorganized by J.P. Morgan in 1901."

{kind=link}

Sunday, March 2, 2014

Stoicism: On Saving Time

What man can you show me who places any value on his time, who reckons the worth of each day, who understands that he is dying daily? For we are mistaken when we look forward to death+; the major portion of death has already passed, Whatever years be behind us are in death's hands.

Therefore, Lucilius, do as you write me that you are doing: hold every hour in your grasp. Lay hold of to-day's task, and you will not need to depend so much upon to-morrow's. While we are postponing,

life speeds by. Nothing, Lucilius, is ours, except time. We were entrusted by nature with the ownership of this single thing, so fleeting and slippery that anyone who will can oust us from possession. What fools these mortals be! They allow the cheapest and most useless things, which can easily be replaced, to be charged in the reckoning, after they have acquired them; but they never regard themselves as in debt when they have received some of that precious commodity, - time! And yet time is the one loan which even a grateful recipient cannot repay.

via: STOICS

Therefore, Lucilius, do as you write me that you are doing: hold every hour in your grasp. Lay hold of to-day's task, and you will not need to depend so much upon to-morrow's. While we are postponing,

life speeds by. Nothing, Lucilius, is ours, except time. We were entrusted by nature with the ownership of this single thing, so fleeting and slippery that anyone who will can oust us from possession. What fools these mortals be! They allow the cheapest and most useless things, which can easily be replaced, to be charged in the reckoning, after they have acquired them; but they never regard themselves as in debt when they have received some of that precious commodity, - time! And yet time is the one loan which even a grateful recipient cannot repay.

via: STOICS

Be the Distruptor

"there has to be a technological core....not per say, but improvement can be brought through sophistication - that has to exist in order for disruption to occur."

H/T : VIW

H/T : VIW

Notes from Buffett's 2008 Berkshire Letter

We're reaching some very high equity market levels, time to look back and reflect if we learned from history. Key Points from Berkshire's 2008 Letter:

Take a look again at the 44-year table on page 2. In 75% of those years, the S&P stocks recorded again. I would guess that a roughly similar percentage of years will be positive in the next 44. But neither Charlie Munger, my partner in running Berkshire, nor I can predict the winning and losing years in advance. (In our usual opinionated view, we don’t think anyone else can either.) We’re certain, for example, that the economy will be in shambles throughout 2009 – and, for that matter, probably well beyond – but that conclusion does not tell us whether the stock market will rise or fall.

In good years and bad, Charlie and I simply focus on four goals:

(1) maintaining Berkshire’s Gibraltar-like financial position, which features huge amounts of

excess liquidity, near-term obligations that are modest, and dozens of sources of earnings

and cash;

(2) widening the “moats” around our operating businesses that give them durable competitive

advantages;

(3) acquiring and developing new and varied streams of earnings;

(4) expanding and nurturing the cadre of outstanding operating managers who, over the years,have delivered Berkshire exceptional results

Berkshire is always a buyer of both businesses and securities, and the disarray in markets gave us a tailwind in our purchases. When investing,pessimism is your friend, euphoria the enemy.

I made at least one major mistake of commission and several lesser ones that also hurt. I will tell you more about these later. Furthermore, I made some errors of omission, sucking my thumb when new facts came in that should have caused me to re-examine my thinking and promptly take action.

Additionally, the market value of the bonds and stocks that we continue to hold suffered a significant decline along with the general market. This does not bother Charlie and me. Indeed, we enjoy such price declines if we have funds available to increase our positions. Long ago, Ben Graham taught me that “Price is what you pay; value is what you get.” Whether we’re talking about socks or stocks, I like buying quality merchandise when it is marked down.

Our long-avowed goal is to be the “buyer of choice” for businesses – particularly those built and owned by families. The way to achieve this goal is to deserve it. That means we must keep our promises; avoid leveraging up acquired businesses; grant unusual autonomy to our managers; and hold the purchased companies through thick and thin (though we prefer thick and thicker).

Our record matches our rhetoric. Most buyers competing against us, however, follow a different path. For them, acquisitions are “merchandise.” Before the ink dries on their purchase contracts, these operators are contemplating “exit strategies.” We have a decided advantage, therefore, when we encounter sellers who truly care about the future of their businesses.

Reinsurance is a business of long-term promises, sometimes extending for fifty years or more. This past year has retaught clients a crucial principle: A promise is no better than the person or institution making it.

That’s where General Re excels: It is the only reinsurer that is backed by an AAA corporation. Ben Franklin once said, “It’s difficult for an empty sack to stand upright.” That’s no worry for General Re clients.

At that time, much of the industry employed sales practices that were atrocious. Writing about the period somewhat later, I described it as involving “borrowers who shouldn’t have borrowed being financed by lenders who shouldn’t have lent.”

Why are our borrowers – characteristically people with modest incomes and far-from-great credit scores – performing so well? The answer is elementary, going right back to Lending 101. Our borrowers simply looked at how full-bore mortgage payments would compare with their actual – not hoped-for – income and then decided whether they could live with that commitment. Simply put, they took out a mortgage with the intention of paying it off, whatever the course of home prices.

Just as important is what our borrowers did not do. They did not count on making their loan payments by means of refinancing. They did not sign up for “teaser” rates that upon reset were outsized relative to their income. And they did not assume that they could always sell their home at a profit if their mortgage payments became onerous. Jimmy Stewart would have loved these folks.

Commentary about the current housing crisis often ignores the crucial fact that most foreclosures do not occur because a house is worth less than its mortgage (so-called “upside-down” loans). Rather, foreclosures take place because borrowers can’t pay the monthly payment that they agreed to pay. Homeowners who have made a meaningful down-payment – derived from savings and not from other borrowing – seldom walk away from a primary residence simply because its value today is less than the mortgage. Instead, they walk when they can’t make the monthly payments.

Home ownership is a wonderful thing. My family and I have enjoyed my present home for 50 years, with more to come. But enjoyment and utility should be the primary motives for purchase, not profit.; the home purchased ought to fit the income of the purchaser.

The present housing debacle should teach home buyers, lenders, brokers and government some simple lessons that will ensure stability in the future. Home purchases should involve an honest-to-God down payment of at least 10% and monthly payments that can be comfortably handled by the borrower’s income. That income should be carefully verified. Putting people into homes, though a desirable goal, shouldn’t be our country’s primary objective. Keeping them in their homes should be the ambition.

“Back-tested” models of many kinds are susceptible to this sort of error. Nevertheless, they are frequently touted in financial markets as guides to future action. (If merely looking up past financial data would tell you what the future holds, the Forbes 400 would consist of librarians.)

Investors should be skeptical of history-based models. Constructed by a nerdy-sounding priesthood using esoteric terms such as beta, gamma, sigma and the like, these models tend to look impressive. Too often, though, investors forget to examine the assumptions behind the symbols. Our advice: Beware of geeks bearing formulas.

However, I have pledged – to you, the rating agencies and myself – to always run Berkshire with more than ample cash. We never want to count on the kindness of strangers in order to meet tomorrow’s obligations. When forced to choose, I will not trade even a night’s sleep for the chance of extra profits.

Clinging to cash equivalents or long-term government bonds at present yields is almost certainly a terrible policy if continued for long. Holders of these instruments, of course, have felt increasingly comfortable – in fact, almost smug – in following this policy as financial turmoil has mounted. They regard their judgment confirmed when they hear commentators proclaim “cash is king,” even though that wonderful cash is earning close to nothing and will surely find its purchasing power eroded over time.

Approval, though, is not the goal of investing. In fact, approval is often counter-productive because it sedates the brain and makes it less receptive to new facts or a re-examination of conclusions formed earlier. Beware the investment activity that produces applause; the great moves are usually greeted by yawns.

Take a look again at the 44-year table on page 2. In 75% of those years, the S&P stocks recorded again. I would guess that a roughly similar percentage of years will be positive in the next 44. But neither Charlie Munger, my partner in running Berkshire, nor I can predict the winning and losing years in advance. (In our usual opinionated view, we don’t think anyone else can either.) We’re certain, for example, that the economy will be in shambles throughout 2009 – and, for that matter, probably well beyond – but that conclusion does not tell us whether the stock market will rise or fall.

In good years and bad, Charlie and I simply focus on four goals:

(1) maintaining Berkshire’s Gibraltar-like financial position, which features huge amounts of

excess liquidity, near-term obligations that are modest, and dozens of sources of earnings

and cash;

(2) widening the “moats” around our operating businesses that give them durable competitive

advantages;

(3) acquiring and developing new and varied streams of earnings;

(4) expanding and nurturing the cadre of outstanding operating managers who, over the years,have delivered Berkshire exceptional results

Berkshire is always a buyer of both businesses and securities, and the disarray in markets gave us a tailwind in our purchases. When investing,pessimism is your friend, euphoria the enemy.

I made at least one major mistake of commission and several lesser ones that also hurt. I will tell you more about these later. Furthermore, I made some errors of omission, sucking my thumb when new facts came in that should have caused me to re-examine my thinking and promptly take action.

Additionally, the market value of the bonds and stocks that we continue to hold suffered a significant decline along with the general market. This does not bother Charlie and me. Indeed, we enjoy such price declines if we have funds available to increase our positions. Long ago, Ben Graham taught me that “Price is what you pay; value is what you get.” Whether we’re talking about socks or stocks, I like buying quality merchandise when it is marked down.

Our long-avowed goal is to be the “buyer of choice” for businesses – particularly those built and owned by families. The way to achieve this goal is to deserve it. That means we must keep our promises; avoid leveraging up acquired businesses; grant unusual autonomy to our managers; and hold the purchased companies through thick and thin (though we prefer thick and thicker).

Our record matches our rhetoric. Most buyers competing against us, however, follow a different path. For them, acquisitions are “merchandise.” Before the ink dries on their purchase contracts, these operators are contemplating “exit strategies.” We have a decided advantage, therefore, when we encounter sellers who truly care about the future of their businesses.

Reinsurance is a business of long-term promises, sometimes extending for fifty years or more. This past year has retaught clients a crucial principle: A promise is no better than the person or institution making it.

That’s where General Re excels: It is the only reinsurer that is backed by an AAA corporation. Ben Franklin once said, “It’s difficult for an empty sack to stand upright.” That’s no worry for General Re clients.

At that time, much of the industry employed sales practices that were atrocious. Writing about the period somewhat later, I described it as involving “borrowers who shouldn’t have borrowed being financed by lenders who shouldn’t have lent.”

Why are our borrowers – characteristically people with modest incomes and far-from-great credit scores – performing so well? The answer is elementary, going right back to Lending 101. Our borrowers simply looked at how full-bore mortgage payments would compare with their actual – not hoped-for – income and then decided whether they could live with that commitment. Simply put, they took out a mortgage with the intention of paying it off, whatever the course of home prices.

Just as important is what our borrowers did not do. They did not count on making their loan payments by means of refinancing. They did not sign up for “teaser” rates that upon reset were outsized relative to their income. And they did not assume that they could always sell their home at a profit if their mortgage payments became onerous. Jimmy Stewart would have loved these folks.

Commentary about the current housing crisis often ignores the crucial fact that most foreclosures do not occur because a house is worth less than its mortgage (so-called “upside-down” loans). Rather, foreclosures take place because borrowers can’t pay the monthly payment that they agreed to pay. Homeowners who have made a meaningful down-payment – derived from savings and not from other borrowing – seldom walk away from a primary residence simply because its value today is less than the mortgage. Instead, they walk when they can’t make the monthly payments.

Home ownership is a wonderful thing. My family and I have enjoyed my present home for 50 years, with more to come. But enjoyment and utility should be the primary motives for purchase, not profit.; the home purchased ought to fit the income of the purchaser.

The present housing debacle should teach home buyers, lenders, brokers and government some simple lessons that will ensure stability in the future. Home purchases should involve an honest-to-God down payment of at least 10% and monthly payments that can be comfortably handled by the borrower’s income. That income should be carefully verified. Putting people into homes, though a desirable goal, shouldn’t be our country’s primary objective. Keeping them in their homes should be the ambition.

“Back-tested” models of many kinds are susceptible to this sort of error. Nevertheless, they are frequently touted in financial markets as guides to future action. (If merely looking up past financial data would tell you what the future holds, the Forbes 400 would consist of librarians.)

Investors should be skeptical of history-based models. Constructed by a nerdy-sounding priesthood using esoteric terms such as beta, gamma, sigma and the like, these models tend to look impressive. Too often, though, investors forget to examine the assumptions behind the symbols. Our advice: Beware of geeks bearing formulas.

However, I have pledged – to you, the rating agencies and myself – to always run Berkshire with more than ample cash. We never want to count on the kindness of strangers in order to meet tomorrow’s obligations. When forced to choose, I will not trade even a night’s sleep for the chance of extra profits.

Clinging to cash equivalents or long-term government bonds at present yields is almost certainly a terrible policy if continued for long. Holders of these instruments, of course, have felt increasingly comfortable – in fact, almost smug – in following this policy as financial turmoil has mounted. They regard their judgment confirmed when they hear commentators proclaim “cash is king,” even though that wonderful cash is earning close to nothing and will surely find its purchasing power eroded over time.

Approval, though, is not the goal of investing. In fact, approval is often counter-productive because it sedates the brain and makes it less receptive to new facts or a re-examination of conclusions formed earlier. Beware the investment activity that produces applause; the great moves are usually greeted by yawns.

Weekend Linkfest

"The Mammoth Cometh" http://rdd.me/tmvcaejn via @readability

"Rolls-Royce Drone Ships Challenge $375 Billion Industry: Freight" http://rdd.me/vxed0tvz via @readability

"While the polar vortex freezes U.S. flights, Nordic airports make sport of defying the snow." http://rdd.me/6eoxjqa9 via @readability

"A Star in a Bottle" http://rdd.me/pksy0oqt via @readability

"Obama's Trauma Team" http://rdd.me/kgygy5ek via @readability

"We Are Less Than Rational" http://rdd.me/mdmdnb93 via @readability

Best Advice: Spot Bad Advice Early In Your Career | LinkedIn http://www.linkedin.com/today/post/article/20140225105559-249493-best-advice-spot-bad-advice-early-in-your-career …

Berkshire Letter 2013 http://www.berkshirehathaway.com/letters/2013ltr.pdf …

Open Strategist: Michael Porter on Value Based Healthcare {video} http://prashantkhorana.blogspot.com/2014/03/michael-porter-on-value-based-healthcare.html?spref=tw …

"Michael Steinhardt, Wall Street's Greatest Trader, Is Back -- And He's Reinventing Investing Again" http://rdd.me/1dytlqxe via @readability

"Twelve legendary investors on what to do with your money now" http://rdd.me/8ogbn0fv via @readability

El-Erian's PIMCO Resignation Memo - Business Insider http://www.businessinsider.com/el-erians-pimco-resignation-memo-2014-2 …

Oddball Stocks: Humility and knowledge http://www.oddballstocks.com/2014/02/humility.html?spref=tw …

"Rolls-Royce Drone Ships Challenge $375 Billion Industry: Freight" http://rdd.me/vxed0tvz via @readability

"While the polar vortex freezes U.S. flights, Nordic airports make sport of defying the snow." http://rdd.me/6eoxjqa9 via @readability

"A Star in a Bottle" http://rdd.me/pksy0oqt via @readability

"Obama's Trauma Team" http://rdd.me/kgygy5ek via @readability

"We Are Less Than Rational" http://rdd.me/mdmdnb93 via @readability

Best Advice: Spot Bad Advice Early In Your Career | LinkedIn http://www.linkedin.com/today/post/article/20140225105559-249493-best-advice-spot-bad-advice-early-in-your-career …

Berkshire Letter 2013 http://www.berkshirehathaway.com/letters/2013ltr.pdf …

Open Strategist: Michael Porter on Value Based Healthcare {video} http://prashantkhorana.blogspot.com/2014/03/michael-porter-on-value-based-healthcare.html?spref=tw …

"Michael Steinhardt, Wall Street's Greatest Trader, Is Back -- And He's Reinventing Investing Again" http://rdd.me/1dytlqxe via @readability

"Twelve legendary investors on what to do with your money now" http://rdd.me/8ogbn0fv via @readability

El-Erian's PIMCO Resignation Memo - Business Insider http://www.businessinsider.com/el-erians-pimco-resignation-memo-2014-2 …

Oddball Stocks: Humility and knowledge http://www.oddballstocks.com/2014/02/humility.html?spref=tw …

Saturday, March 1, 2014

Highlights from Berkshire's 2013 letter

Here are some highlights extracted from the 2013 letter:

Over the stock market cycle between

yearends 2007 and 2013, we overperformed the S&P. Through full cycles in

future years, we expect to do that again. If we fail to do so, we will not have

earned our pay. After all, you could always own an index fund and be assured of

S&P results.

Though the

Heinz acquisition has some similarities to a “private equity” transaction,

there is a crucial difference: Berkshire never intends to sell a share of the

company. What we would like, rather, is to buy more, and that could happen:

Certain 3G investors may sell some or all of their shares in the future, and we

might increase our ownership at such times. Berkshire and 3G could also decide

at some point that it

would be

mutually beneficial if we were to exchange some of our preferred for common

shares (at an equity valuation appropriate to the time).

With Heinz, Berkshire now owns 81/2

companies that, were they stand-alone businesses, would be in the Fortune

500. Only 4911/2 to go.

Berkshire’s extensive insurance operation

again operated at an underwriting profit in 2013 – that makes 11years in a row

– and increased its float. During that 11-year stretch, our float – money that

doesn’t belong to us but that we can invest for Berkshire’s benefit – has grown

from $41 billion to $77 billion.

While Charlie and I search for elephants,

our many subsidiaries are regularly making bolt-on acquisitions.Last year, we contracted for 25 of these,

scheduled to cost $3.1 billion in aggregate. These transactions ranged from

$1.9 million to $1.1 billion in size.

Charlie and I encourage these deals. They deploy capital in activities that fit with our

existing businesses and that will be managed by our corps of expert managers.

The result is no more work for us and more earnings for you. Many more of these

bolt-on deals will be made in future years. In aggregate, they will be meaningful.

In a year in which most equity managers

found it impossible to outperform the S&P 500, both Todd Combs and Ted

Weschler handily did so. Each now runs a portfolio exceeding $7 billion.

They’ve earned it .I must again confess that their investments outperformed

mine. (Charlie says I should add “by a lot.”) If such humiliating comparisons

continue, I’ll have no choice but to cease talking about them.

Todd and Ted have also created significant

value for you in several matters unrelated to their portfolio activities. Their

contributions are just beginning: Both men have Berkshire blood in their veins.

And, if you think tenths of a percent

aren’t important, ponder this math: For the four companies in aggregate, each

increase of one-tenth of a percent in our share of their equity raises

Berkshire’s share of their annual earnings by $50 million.

The four companies possess excellent

businesses and are run by managers who are both talented and shareholder-oriented.

At Berkshire, we much prefer owning a non-controlling but substantial portion

of a wonderful company to owning 100% of a so-so business; it’s better to have a partial

interest in the Hope diamond than to own all of a rhinestone.

Our flexibility in capital allocation –

our willingness to invest large sums passively in non-controlled businesses –

gives us a significant advantage over companies that limit themselves to

acquisitions they can operate. Woody

Allen stated the general idea when he said: “The advantage of being bi-sexual

is that it doubles your chances for a date on Saturday night.” Similarly,

our appetite for either operating businesses or passive investments

doubles our chances of finding sensible uses for our endless gusher of cash.

Indeed, who has ever benefited during the

past 237 years by betting against America? If you compare our country’s present

condition to that existing in 1776, you have to rub your eyes in wonder. And

the dynamism embedded in our market economy will continue to work its magic.

America’s best days lie ahead.

With this tailwind working for us, Charlie and I hope to build

Berkshire’s per-share intrinsic value by:

(1) constantly improving the basic earning

power of our many subsidiaries;

(2) further increasing their earnings

through bolt-on acquisitions;

(3) benefiting from the growth of our

investees;

(4) repurchasing Berkshire shares when

they are available at a meaningful discount from intrinsic value; and (5)

making an occasional large acquisition. We will also try to maximize results

for you by rarely, if ever, issuing Berkshire shares.

Though individual policies and claims come

and go, the amount of float an insurer holds usually remains fairly stable in

relation to premium volume.

If our premiums exceed the total of our

expenses and eventual losses, we register an underwriting profit that adds to

the investment income our float produces. When such a profit is earned, we

enjoy the use of free money – and, better yet, get paid for holding it.

Looking ahead, I believe we will continue

to underwrite profitably in most years. Doing so is the daily focus of all of

our insurance managers who know that while float is valuable, it can be drowned

by poor underwriting results.

Just as surely, we each day write new

business and thereby generate new claims that add to float. If our revolving

float is both costless and long-enduring, which I believe it will be, the true

value of this liability is dramatically less than the accounting liability.

A counterpart to this overstated liability

is $15.5 billion of “goodwill” that is attributable to our insurance companies

and included in book value as an asset. In very large part, this goodwill

represents the price we paid for the float-generating capabilities of our

insurance operations. The cost of the goodwill, however, has no bearing on its

true value. For example, if an insurance business sustains large and prolonged

underwriting losses, any goodwill asset carried on the books should be deemed

valueless, whatever its original cost. Fortunately, that does not describe

Berkshire. Charlie and I believe the true economic value of our insurance

goodwill – what we would happily pay to purchase an insurance operation

possessing float of similar quality to that we have – to be far in excess of

its historic carrying value. The

value of our float is one reason – a huge reason – why we believe Berkshire’s

intrinsic business value substantially exceeds its book value.

I won’t explain all of the adjustments –

some are tiny and arcane – but serious investors should understand the

disparate nature of intangible assets: Some truly deplete over time while

others in no way lose value. With software, for example, amortization charges

are very real expenses. Charges against other intangibles such as the

amortization of customer relationships, however, arise through

purchase-accounting rules and are clearly not real costs. GAAP accounting draws

no distinction between the two types of charges. Both, that is, are recorded as

expenses when earnings are calculated – even though from an investor’s

viewpoint they could not be more different.

Every dime of depreciation expense we

report, however, is a real cost. And that’s true at almost all other companies

as well. When Wall

Streeters tout EBITDA as a valuation guide, button your wallet. Our public reports of earnings

will, of course, continue to conform to GAAP. To embrace reality, however,

remember to add back most of the amortization charges we report.

Charlie and I believe that all

shareholders should have access to new Berkshire information simultaneously and

should also have adequate time to analyze it. That’s why we try to issue

financial information late on Fridays or early on Saturdays and why our annual

meeting is held on Saturdays. We do not talk one-on-one to large institutional

investors or analysts, but rather treat all shareholders the same. Our hope is

that the journalists and analysts will ask questions that further educate our

owners about their investment.

ON NFM:

I think back to August 30, 1983 – my

birthday – when I went to see Mrs. B (Rose Blumkin), carrying a 11/4-page

purchase proposal for NFM that I had drafted. (It’s reproduced on pages 114 -

115.) Mrs. B accepted my offer without changing a word, and we completed the

deal without the involvement of investment bankers or lawyers (an experience

that can only be described as heavenly). Though the company’s financial

statements were unaudited, I had no worries. Mrs. B simply told me what was

what, and her word was good enough for me. Mrs. B was 89 at the time and worked

until 103 – definitely my kind of woman. Take a look at NFM’s financial

statements from 1946 on pages 116 - 117. Everything NFM now owns comes from (a)

that $72,264 of net worth and $50 – no zeros omitted – of cash the company then

possessed, and (b) the incredible talents of Mrs. B, her son, Louie, and his

sons Ron and Irv.

The punch line to this story is that Mrs.

B never spent a day in school. Moreover, she emigrated from Russia to America

knowing not a word of English. But she loved her adopted country: At Mrs. B’s

request, the family always sang God Bless America at its gatherings.

Aspiring business managers should look

hard at the plain, but rare, attributes that produced Mrs. B’s incredible

success. Students from 40 universities visit me every year, and I have them

start the day with a visit to NFM. If they absorb Mrs. B’s lessons, they need

none from me.

Most of you have never heard of Energy

Future Holdings. Consider yourselves lucky; I certainly wish I hadn’t. The

company was formed in 2007 to effect a giant leveraged buyout of electric

utility assets in Texas. The equity owners put up $8 billion and borrowed a

massive amount in addition. About $2 billion of the debt was purchased by

Berkshire, pursuant to a decision I made without consulting with Charlie. That

was a big mistake.

Unless natural gas prices soar, EFH will almost certainly file for

bankruptcy in 2014. Last year, we sold our holdings for $259 million. While

owning the bonds, we received $837 million in cash interest. Overall, therefore,

we suffered a pre-tax loss of $873 million. Next time I’ll call Charlie.

I tell these tales to illustrate certain

fundamentals of investing:

You don’t need to be an expert in order to

achieve satisfactory investment returns. But if you aren’t, you must recognize

your limitations and follow a course certain to work reasonably well. Keep

things simple and don’t swing for the fences. When

promised quick profits, respond with a quick “no.”

Focus on the future productivity of the

asset you are considering. If you don’t feel comfortable making a

rough estimate of the asset’s future earnings, just forget it and move on. No

one has the ability to evaluate every investment possibility. But omniscience isn’t necessary;

you only need to understand the actions you undertake

If you instead focus on the prospective

price change of a contemplated purchase, you are speculating. There is nothing

improper about that. I know, however, that I am unable to speculate

successfully, and I am skeptical of those who claim sustained success at doing

so. Half of all coin-flippers will win their first toss; none of those winners

has an expectation of profit if he continues to play the game. And the fact

that

a given asset has appreciated in the

recent past is never a reason to buy it.

With my two small investments, I thought

only of what the properties would produce and cared not at all about their

daily valuations. Games are

won by players who focus on the playing field – not by those whose eyes are

glued to the scoreboard. If you can enjoy Saturdays and Sundays without looking

at stock prices, give it a try on weekdays.

Forming macro opinions or listening to the

macro or market predictions of others is a waste of time. Indeed, it is dangerous because it may

blur your vision of the facts that are truly important.

...if a moody fellow with a farm bordering

my property yelled out a price every day to me at which he would either buy my

farm or sell me his – and those prices varied widely over short periods of time

depending on his mental state – how in the world could I be other than

benefited by his erratic behavior? If his daily shout-out was ridiculously low,

and I had some spare cash, I would buy his farm. If the number he yelled was

absurdly high, I could either sell to him or just go on farming.

Those people who can sit quietly for

decades when they own a farm or apartment house too often become frenetic when

they are exposed to a stream of stock quotations and accompanying commentators

delivering an implied message of “Don’t just sit there, do something.” For

these investors, liquidity is

transformed from the unqualified benefit it should be to a curse.

A “flash crash” or some other extreme

market fluctuation can’t hurt an investor any more than an erratic and

mouthy neighbor can hurt my farm investment. Indeed, tumbling markets can be helpful to

the true investor if he has cash available when prices get far out of line with

values. A climate of fear is

your friend when investing; a euphoric world is your enemy.

Most investors, of course, have not made

the study of business prospects a priority in their lives. If wise, they will

conclude that they do not know enough about specific businesses to predict

their future earning power.

I can’t remember what I paid for that

first copy of The Intelligent Investor. Whatever the cost, it would underscore

the truth of Ben’s adage:

Price is what you pay, value is what you get. Of

all the investments I ever made, buying Ben’s book was the best (except for my

purchase of two marriage licenses).

Full letter : BRK

Subscribe to:

Comments (Atom)